Triple-Net Retail REIT Update – May 2026

May 12, 2026

Triple-Net Retail REIT Update: Institutional Capital Continues to Favor Defensive Retail Assets

The triple-net retail REIT sector entered 2026 from a position of strength.

Despite ongoing economic uncertainty, cautious consumer sentiment, and elevated interest rates, net-leased retail REITs continued to demonstrate resilience through stable occupancy, disciplined acquisition activity, and durable cash flow generation. Capright’s newly released Triple-Net Retail REIT Update examines the evolving dynamics shaping the sector and why institutional capital continues to gravitate toward high-credit, necessity-based retail assets.

Please enter your email to download the report

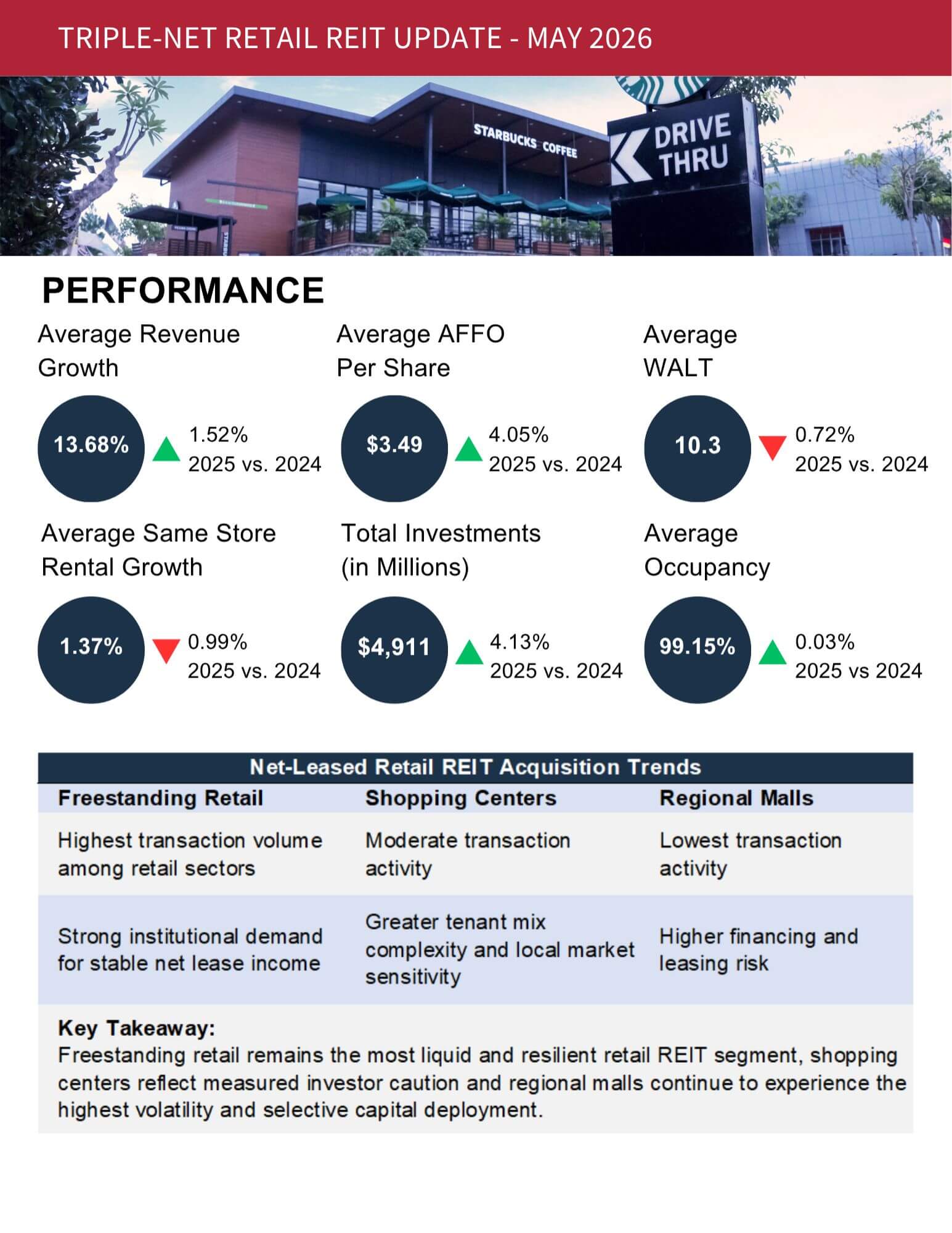

Strong Fundamentals Continue to Support the Sector

The update highlights several key operating metrics demonstrating the stability of the net-lease retail space:

- Average occupancy across major retail REITs remained above 99%

- Average weighted average lease terms (WALT) exceeded 15 years

- Average AFFO per share growth reached 4.05%

- Revenue growth remained healthy despite a more selective capital markets environment

These metrics reinforce why net-leased retail assets continue to be viewed as one of the most defensive segments within commercial real estate.

Unlike more operationally intensive retail formats, triple-net retail properties benefit from long lease durations, reduced landlord responsibilities, and stronger income predictability. This has become increasingly attractive in an environment where investors are prioritizing durability, transparency, and stable cash flow.

Acquisition Activity Accelerated Throughout 2025

One of the update’s central themes is the resurgence in acquisition activity.

According to Marcus & Millichap data cited in the update, single-tenant net-lease retail transaction volume increased 17% YoY during 2025, reflecting renewed investor appetite for stable income-producing assets.

Major institutional REITs including:

- Realty Income (O)

- NNN REIT (NNN)

- Agree Realty (AGR)

- Essential Properties (EPRT)

continued to scale acquisition platforms while maintaining disciplined underwriting standards and conservative capital structures. Combined, these REITs executed more than $4.9B in acquisitions during the year.

Credit Quality Is Driving Pricing Divergence

Premium investment-grade tenants continue to command aggressive pricing, with select ground-leased assets trading below 4.50% cap rates. Meanwhile, challenged retail operators, including certain pharmacy tenants, are trading well above 7.00%.

This divergence reflects a broader market trend:

Institutional investors are increasingly concentrating capital into durable, necessity-based retail concepts with predictable cash flows and stronger rent coverage.

As a result, pricing for top-tier assets has remained relatively insulated from broader cap rate expansion, while weaker credit assets continue to reprice more materially.

Freestanding Retail Continues to Outperform Other Retail Formats

Capright’s update also compares performance trends across:

- freestanding retail,

- shopping centers,

- and regional malls.

The analysis shows freestanding retail continues to generate substantially more transaction activity than the other sectors due to:

- smaller asset sizes,

- single-tenant simplicity,

- lower price points,

- and stronger institutional demand for stable net lease income.

While shopping centers and regional malls continue to face greater leasing complexity and volatility, freestanding retail has maintained stronger pricing resilience and liquidity.

This reinforces the sector’s role as a defensive anchor within institutional retail portfolios.

Looking Ahead

The report concludes that while capital markets remain selective, the net lease retail sector remains well-positioned for continued stability and long-term growth.

REITs with:

- disciplined balance sheet management,

- scalable acquisition platforms,

- strong tenant relationships,

- and conservative underwriting

are expected to remain best positioned to navigate evolving market conditions.

As investors continue prioritizing income durability and operational resilience, triple-net retail assets remain among the most attractive allocations within the broader CRE landscape.

📬 Let’s Talk

At Capright, we are uniquely positioned to support institutional investors, operators, and developers navigating this evolving environment. As an independent valuation and advisory firm, we provide clarity, accuracy, and confidence, especially where the stakes are highest.

If you’d like to discuss the findings or need support with your commercial real estate valuation or strategy, reach out to:

Principal

📧 koxtal@capright.com

🔗 Connect on LinkedIn

Senior Associate

📧 jticus@capright.com

🔗 Connect on LinkedIn