Data Center Market Update – April 2026

April 13, 2026

Data Center Market Update: Power Constraints, Capital Flows, and the Next Phase of Growth

The U.S. data center market is entering a new chapter. One defined not by lack of demand, but by the increasing complexity of delivering supply.

Capright’s Data Center Market Update – April 2026 highlights a market still experiencing strong financial performance and investor interest, yet facing real constraints around power, regulation, and speed to delivery.

Please enter your email to download the report

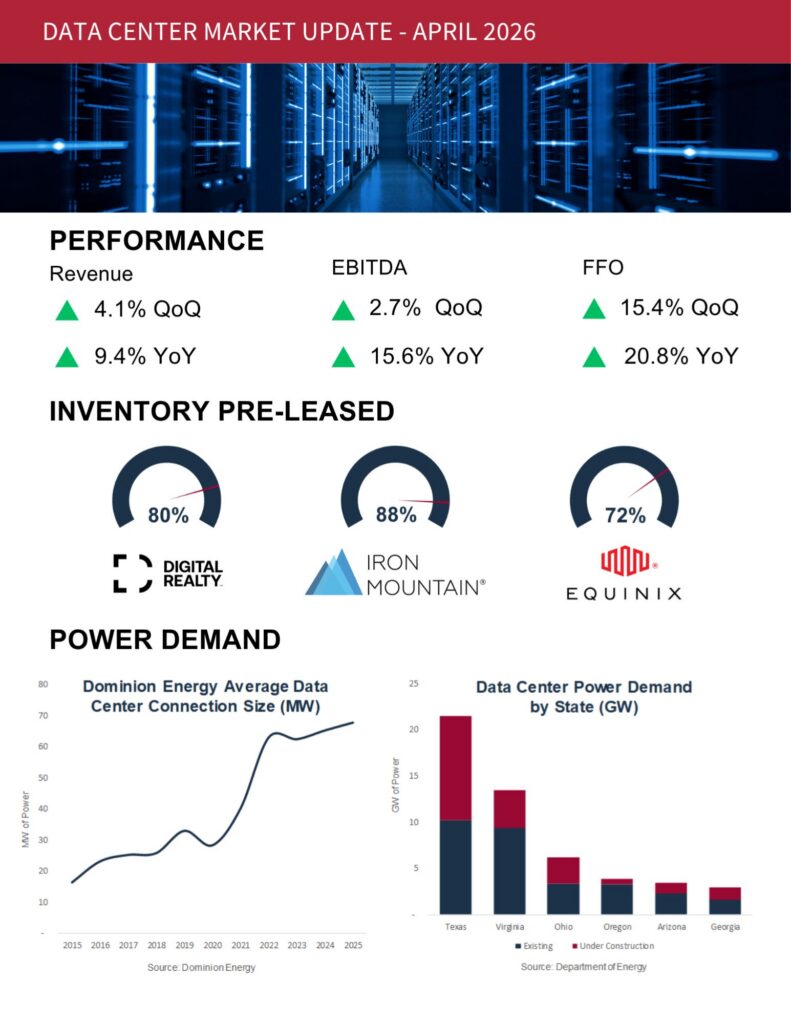

Key Performance Trends: Growth Remains Strong

Despite broader market challenges, operating fundamentals remain robust:

- Revenue: +4.1% QoQ

- EBITDA: +2.7% QoQ

- FFO: +15.4% QoQ

These figures underscore continued demand from hyperscale users and AI-driven workloads, reinforcing data centers as one of the strongest-performing asset classes in CRE.

Power Is the New Bottleneck

The biggest constraint facing the sector is no longer capital, it’s power availability.

- Utility timelines are now 1.5 to 2 years longer than developer expectations

- Developers are shifting toward behind-the-meter and hybrid power solutions

- Competition for sites with immediate power access is intensifying

This dynamic is fundamentally reshaping development strategy and site selection.

Construction Deceleration, Not Demand Decline

After years of rapid expansion, the market experienced construction deceleration at the end of 2025. The first pullback in new capacity since 2020.

This slowdown is not demand-driven. Instead, it reflects:

- Increased regulatory scrutiny

- Longer entitlement timelines

- Community pushback in core markets

As a result, developers are prioritizing “ready-to-build” sites with power and approvals already in place.

Geographic Shift: Texas Takes the Lead

A notable shift is underway in where data centers are being built:

- Texas has surpassed Northern Virginia in total power demand

- Markets like Dallas-Fort Worth, Austin, and San Antonio are gaining momentum

- Northern Virginia remains dominant, but faces zoning and entitlement constraints

Access to scalable power and flexible regulation is driving this geographic rebalancing.

Capital Deployment Remains Aggressive

Even as development becomes more complex, capital continues to flow into the sector:

- $20B multi-building campus partnership (Hillwood & PowerHouse)

- $2B investment into AI infrastructure (NVIDIA & CoreWeave)

- 1.4 GW “Stargate” campus backed by OpenAI, Oracle, and Related Digital

At the same time, land pricing reflects scarcity:

- Northern Virginia land trades reached $6.3M per acre, a new high-water mark

Development Pipeline: Pre-Leasing Signals Strength

Demand visibility remains exceptionally strong:

- Digital Realty: 523 MW under construction, 80% pre-leased

- Iron Mountain: 134 MW, 88% pre-leased

- Equinix: 158 MW, 72% pre-leased

High pre-leasing levels indicate that supply constraints, not demand, will continue to define near-term market dynamics.

Valuation & Capital Markets Context

- Data center REIT implied cap rates have declined 66 bps since 2022 peak

- Interest rate volatility remains a factor, with the 10-year Treasury fluctuating between 3.97% and 4.40%

While capital markets remain supportive, macro conditions continue to influence pricing and underwriting assumptions.

📬 Let’s Talk

At Capright, we are uniquely positioned to support institutional investors, operators, and developers navigating this evolving environment. As an independent valuation and advisory firm, we provide clarity, accuracy, and confidence, especially where the stakes are highest.

If you’d like to discuss the findings or need support with your Data Center valuation or strategy, reach out to:

Principal

📧 dticus@capright.com

🔗 Connect on LinkedIn

Principal

📧 koxtal@capright.com

🔗 Connect on LinkedIn

Director

📧 slore@capright.com

🔗 Connect on LinkedIn