Single-Family Rental REIT Update – May 2026

May 4, 2026

Single-Family Rental REIT Update: Policy Shifts, Supply Dynamics & What Comes Next

Capright is pleased to release its latest Single-Family Rental REIT Update, offering a data-driven look at one of the most closely watched sectors in commercial real estate.

As institutional capital, housing policy, and supply dynamics continue to collide, the Single-Family Rental (SFR) sector sits at the center of a rapidly evolving landscape. This update breaks down what’s happening now, and what investors should be watching next.

Please enter your email to download the report

A Sector on Stable Ground. But Facing a New Cycle

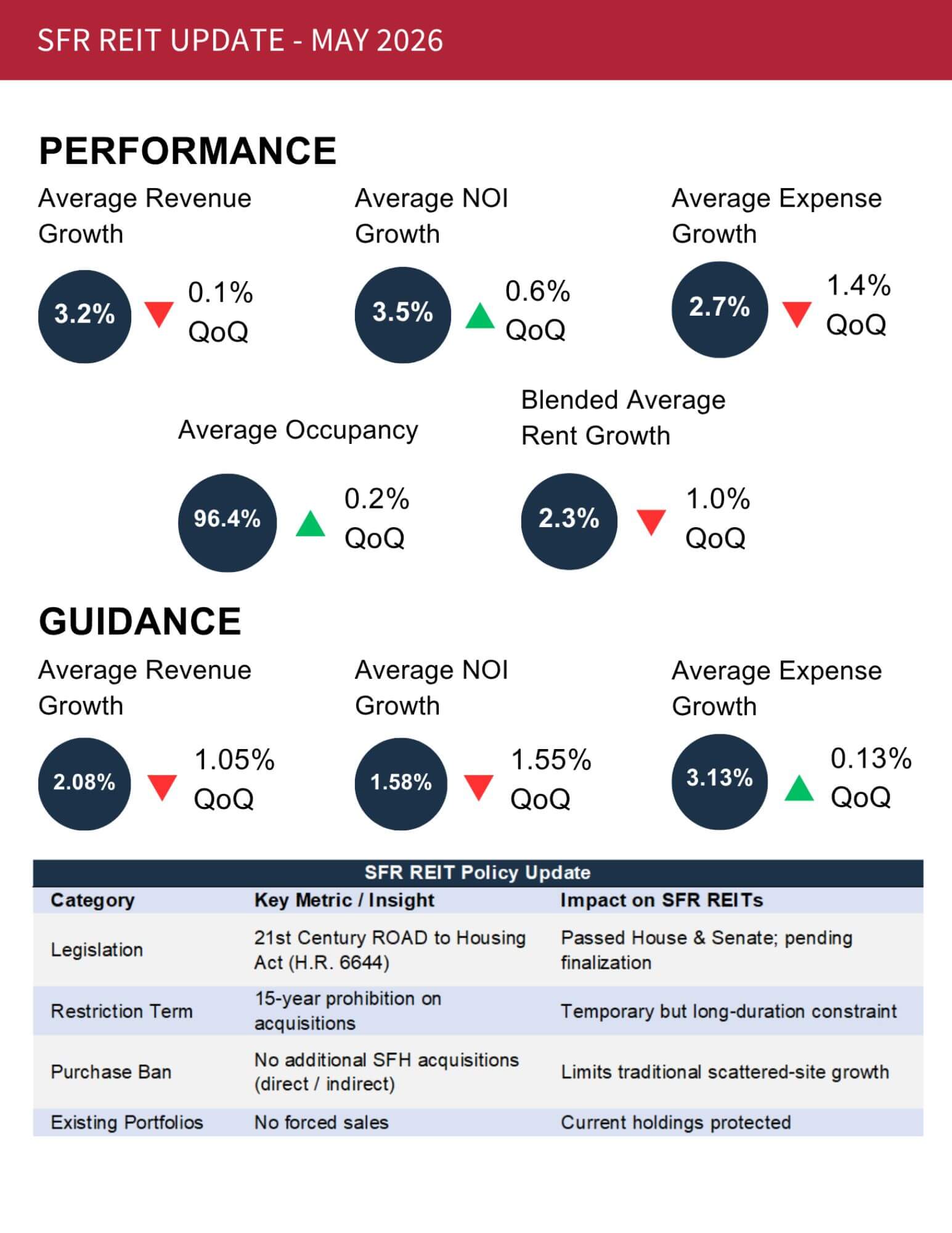

The SFR sector closed 2025 with positive revenue and NOI growth, supported by strong renewal performance and tenant stickiness across major platforms like Invitation Homes (INVH) and American Homes 4 Rent (AMH).

- Average occupancy remains strong at 96.4%

- Blended rent growth: 2.3%

- Renewal rent growth continues to exceed 4%

However, the story is becoming more nuanced. A bifurcated leasing environment has emerged:

- Renewals remain resilient

- New lease rates are under pressure due to elevated supply, particularly in the Sun Belt

This divergence is shaping near-term performance expectations across the sector.

Supply Reset Is Underway

After a surge in Build-to-Rent (BTR) development, the pipeline is beginning to normalize.

- BTR starts declined 19% YoY in 2025

- Development activity is moderating further into 2026

This shift is critical. As supply pressure eases, it sets the stage for:

- Improved pricing power on new leases

- More balanced operating conditions into late 2026 and 2027

The medium-term outlook remains constructive, supported by a structural U.S. housing shortage estimated at 1–4 million units.

Institutional Strategy Is Evolving

One of the most important takeaways: institutional SFR strategies have already changed, independent of policy pressure.

REITs are:

- Moving away from MLS acquisitions

- Prioritizing builder partnerships and internal development

- Increasing dispositions to individual homeowners

This is not theoretical. It’s already happening:

- AMH sold over 1,800 homes to individuals in 2025

- INVH sourced 100% of 4Q25 acquisitions from homebuilders

The implication: the industry is structurally shifting toward development-led growth models.

Policy Spotlight: The 21st Century ROAD to Housing Act

Housing policy moved from headlines to legislation in 1Q26.

The proposed bill:

- Targets institutional ownership of single-family homes

- Imposes a temporary 15-year restriction on new acquisitions for large investors

- Leaves existing portfolios intact

But here’s the key insight:

The largest REITs are already operating in ways largely aligned with the bill’s exemptions.

Builder-driven acquisitions, BTR development, and structured pathways to homeownership are all explicitly permitted under the legislation.

This helps explain why:

- The initial market reaction was sharp

- But longer-term implications may be more limited than headlines suggest

The Bigger Picture: Why SFR Still Matters

Despite near-term noise, the long-term thesis remains intact:

- Renting is still $12,000/year cheaper than owning across REIT markets

- Institutional ownership remains 3% of total SFR stock

- Demand continues to be driven by affordability constraints and demographic shifts

SFR is serving a dual role:

1. A durable income-generating asset class for investors

2. A critical housing solution for a growing renter population

📬 Let’s Talk

At Capright, we are uniquely positioned to support institutional investors, operators, and developers navigating this evolving environment. As an independent valuation and advisory firm, we provide clarity, accuracy, and confidence, especially where the stakes are highest.

If you’d like to discuss the findings or need support with your commercial real estate valuation or strategy, reach out to:

Principal

📧 koxtal@capright.com

🔗 Connect on LinkedIn