Single-Family Rental REIT Update – January 2026

January 19, 2026

Please enter your email to download the report

Resilience Through Repricing – Single-Family Rental REIT Update – 2026

The single-family rental (SFR) sector continues to demonstrate durability as it transitions from a period of rapid growth into a more normalized operating environment. Capright’s Single-Family Rental REIT Update – January 2026 examines how leading public SFR REITs are navigating elevated supply in select markets, policy-driven headline risk, and shifting rent dynamics, while maintaining strong long-term fundamentals.

Resilient Fundamentals Amid Market Complexity

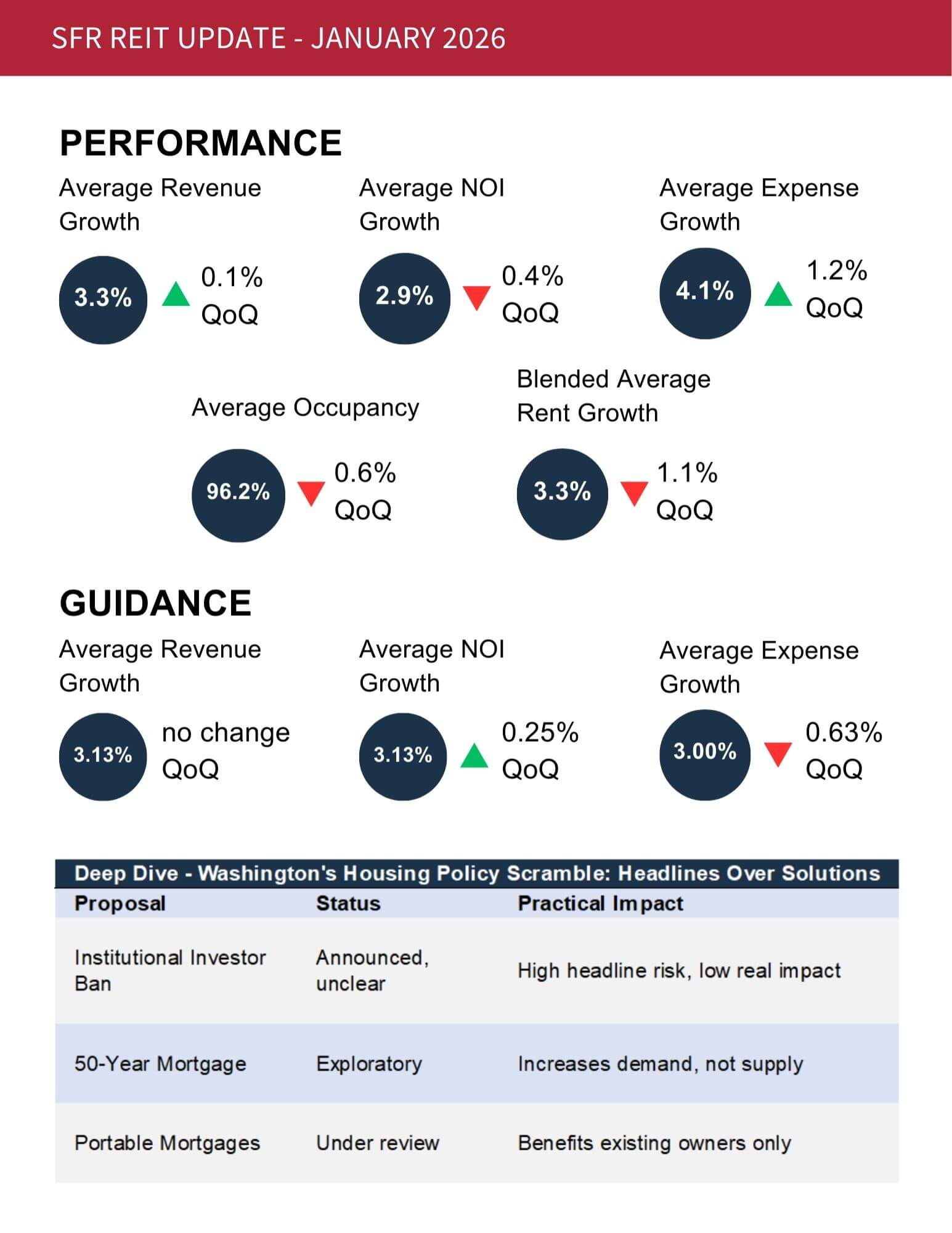

Through 3Q25, public SFR REITs delivered solid YOY performance despite localized pressure from new deliveries. Occupancies remained near 96%, renewal rent growth stayed healthy, and average resident tenure extended beyond 40 months, underscoring strong renter demand and tenant stickiness. NOI results diverged modestly across platforms, driven primarily by expense management, lease-expiration strategy, and market-level supply conditions rather than structural weakness.

Disciplined Growth and Capital Allocation

Acquisition activity remains selective, with REITs favoring builder partnerships, forward purchase agreements, and development-oriented strategies over volume-driven expansion. Invitation Homes and American Homes 4 Rent both raised forward guidance, reflecting confidence in portfolio performance and improved visibility into operating costs. Development pipelines remain active but disciplined, with mid-5% initial yields and funding largely supported by internal capital generation.

Institutional Capital Continues to Expand

Institutional participation in SFR continues to deepen. NCREIF funds increased SFR exposure by more than 20% YOY, yet the asset class still represents just over 3% of total residential exposure, highlighting meaningful runway for future allocation. Competition from private equity platforms remains strong, particularly in Sun Belt and Midwest markets, reinforcing SFR’s position as a core institutional housing strategy.

Rent Growth Normalizes, Renewals Lead

Blended rent growth moderated to the low-3% range, reflecting competitive new-lease conditions in certain markets. Renewal rent growth, however, remained a key driver of performance, supported by low turnover and improving tenant retention. The Midwest emerged as a standout region, benefiting from affordability, limited new supply, and consistent household formation.

Policy Noise vs. Structural Reality

The update’s policy analysis concludes that recent housing proposals largely stimulate demand without addressing the core constraint: supply. Institutional SFR capital has increasingly functioned as housing manufacturing capital through development and forward-purchase structures, positioning the sector to adapt rather than retreat in response to regulatory uncertainty.

The Bigger Picture

The update reinforces the long-term investment case for SFR housing. With leasing remaining materially cheaper than owning in many markets, BTR starts declining sharply from peak levels, and housing undersupply persisting nationwide, the SFR sector is well positioned to deliver durable income for investors while addressing critical affordability gaps heading into 2026.

📬 Let’s Talk

At Capright, we are uniquely positioned to support institutional investors, operators, and developers navigating this evolving environment. As an independent valuation and advisory firm, we provide clarity, accuracy, and confidence, especially where the stakes are highest.

If you’d like to discuss the findings or need support with your Single-Family Rental valuation or strategy, reach out to:

Principal

📧 koxtal@capright.com

🔗 Connect on LinkedIn