Self-Storage REIT Update – June 2026

June 1, 2026

Self-Storage REITs Enter a New Phase of Stabilization Amid Ongoing Pricing Pressure

Capright has released its latest Self-Storage REIT Update, providing a detailed look at the evolving fundamentals shaping the self-storage sector.

After several quarters of normalization, the industry is beginning to show credible signs of stabilization. Occupancy levels have largely held steady, development pipelines continue to thin, and customer retention trends are improving. However, operators remain under pressure as revenue growth slows and expenses continue to rise.

Please enter your email to download the report

Occupancy Stabilizes While Revenue Growth Remains Muted

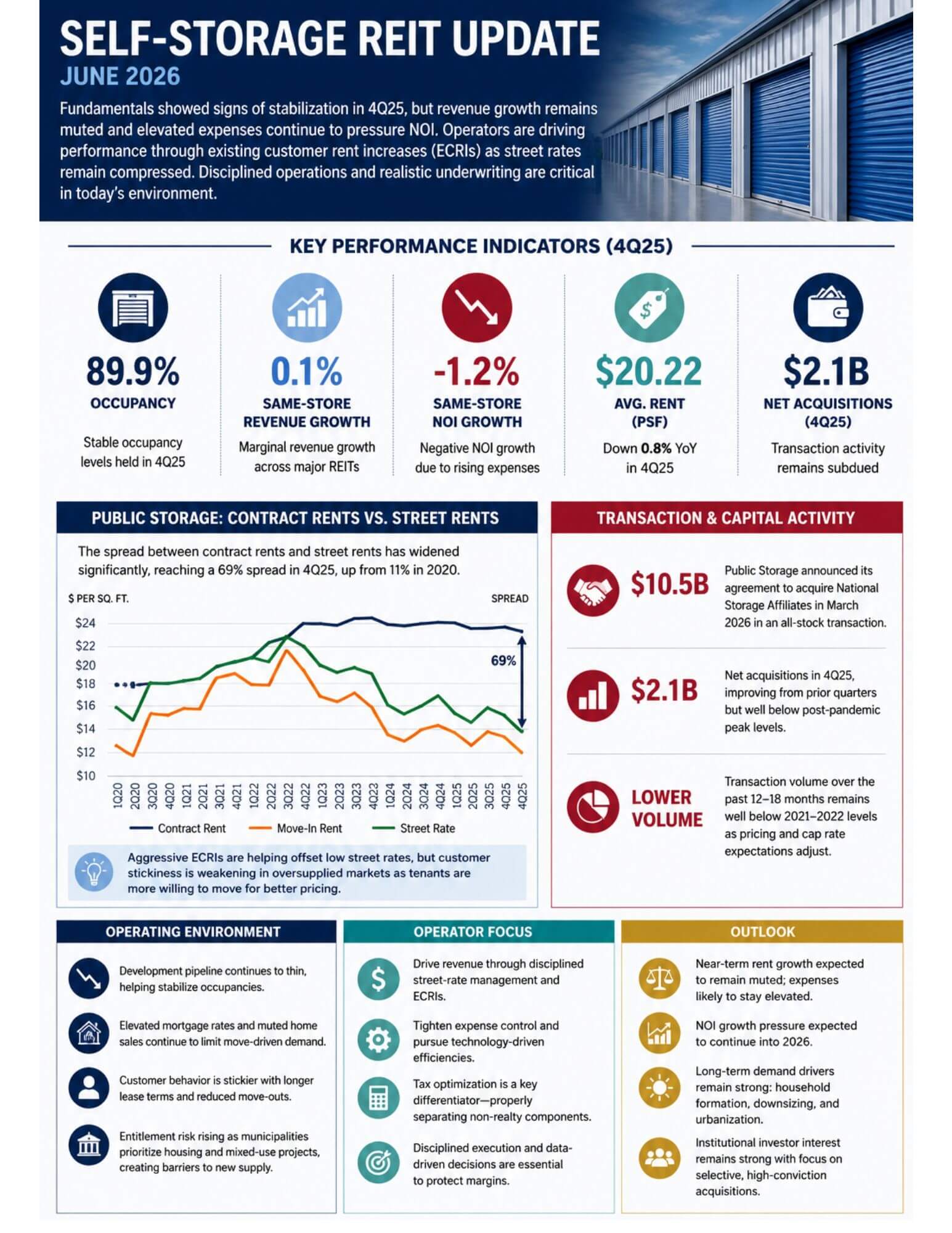

As of 4Q25, average occupancy across the major self-storage REITs stood at 89.9%, remaining largely aligned with historical norms despite broader market headwinds.

At the same time, operators are increasingly relying on existing customer rate increases (ECRIs) to support revenue as street rates remain compressed due to competition and slowing housing activity. This shift is fundamentally changing underwriting assumptions across the sector.

Capright’s update highlights that:

- Same-store revenue growth averaged just 0.1%

- Same-store NOI growth averaged -1.2%

- Rental rates declined 0.8% YoY

- Operators continue facing elevated expense growth across portfolios

The Growing Gap Between Street Rates and Contract Rents

One of the update’s most notable findings is the widening disconnect between street rates and in-place contractual rents.

Capright’s analysis of Public Storage data shows the spread between contract rents and street rents expanded from 11% in 2020 to 69% in 4Q25.

This trend reflects operators aggressively discounting move-in pricing to attract tenants while continuing to push rate increases on existing customers. According to the update, that strategy is beginning to show signs of strain in oversupplied markets where customer mobility is increasing.

Supply Constraints Continue to Shape Market Performance

Capright notes that self-storage performance remains highly market dependent.

Sunbelt markets continue to experience oversupply pressures and rent compression, while supply-constrained gateway markets are stabilizing faster due to development barriers and zoning limitations.

For example:

- New York reported some of the highest rental rates nationally at $33.62 per square foot

- Atlanta continued to face elevated concessions and some of the lowest advertised rents in the sector

The update also emphasizes that entitlement risk and municipal resistance to new self-storage development are becoming increasingly important underwriting considerations as cities prioritize housing and mixed-use projects over storage development.

Institutional Capital Remains Active

Despite softer operating fundamentals, institutional interest in the self-storage sector remains strong.

Capright highlights Public Storage’s planned acquisition of National Storage Affiliates in an approximately $10.5B all-stock transaction as one of the sector’s most significant recent developments.

The update also notes continued institutional portfolio activity across high-growth markets, even as transaction volume remains below peak levels due to interest rates and economic uncertainty.

Outlook for the Self-Storage Sector

Looking ahead, Capright expects near-term NOI pressure to continue as operators balance slowing rent growth with rising expenses. However, long-term fundamentals remain supported by durable demand drivers including household formation, downsizing trends, and ongoing urbanization.

The update concludes that disciplined operations, technology-driven revenue management, and realistic underwriting assumptions will remain critical differentiators for investors and operators navigating the next phase of the self-storage cycle.

Read the full update to explore detailed KPI trends, acquisition activity, occupancy metrics, rental rate analysis, and institutional transaction insights shaping the self-storage REIT landscape in 2026.

📬 Let’s Talk

At Capright, we are uniquely positioned to support institutional investors, operators, and developers navigating this evolving environment. As an independent valuation and advisory firm, we provide clarity, accuracy, and confidence, especially where the stakes are highest.

If you’d like to discuss the findings or need support with your commercial real estate valuation or strategy, reach out to:

Principal

📧 koxtal@capright.com

🔗 Connect on LinkedIn